Member Sign In

Username

Password

Remember me

Lost Password

Sign In

Close

Consensus ESG Ratings

Our ESG Solutions

Corporate Managers

Consultants

Supply Chain Professionals

Investment Professionals

Nonprofit and Government

Academic Researchers

API Developers

Get Started

Advanced Search

How We Generate ESG Ratings

Our data schema

Our ratings methodology

FAQ

How To's

Our data sources

Insight & News

Blog

Research

Strategic Partners

CSRHub Blog

» Latest Articles

Categories

ESG Investing

Corporate Sustainability Metrics

ESG Data Partnerships

ESG Metrics Research

ESG App Development

CSRHub Co-Founder Speaking Events

Cynthia Figge

Bahar Gidwani

CSR

Sustainability

Environment

Social

Governance

Impact

CSRHub Blog

Dec 21, 2022

•

1 min read

Drucker Institute, ESG Investing, ESG score, Corporate Sustainability Metrics, ESG Metrics Research, WSJ Management Top 250

Drucker Institute 2022 Management Top 250 Rankings includes CSRHub Metrics

By CSRHub Blogging

Dec 21, 2022

•

3 min read

governance, social, environment, ESG Metrics Research, impact

The Paradox of ESG

By CSRHub Blogging

Dec 15, 2022

•

4 min read

ESG Investing, ESG App Development, Corporate Sustainability Metrics, ESG Metrics Research

CSRHub Releases Version 3.0 of RESTful Application Programming Interface

By CSRHub Blogging

Dec 08, 2022

•

3 min read

CSR, social, ESG Investing, Corporate Sustainability Metrics, ESG Metrics Research, ESG Data Partnerships

Legacy & CSRHub ESG Media Partnership

By CSRHub Blogging

Nov 16, 2022

•

3 min read

ESG Investing, ESG App Development, Corporate Sustainability Metrics, ESG Metrics Research, ESG Data Partnerships

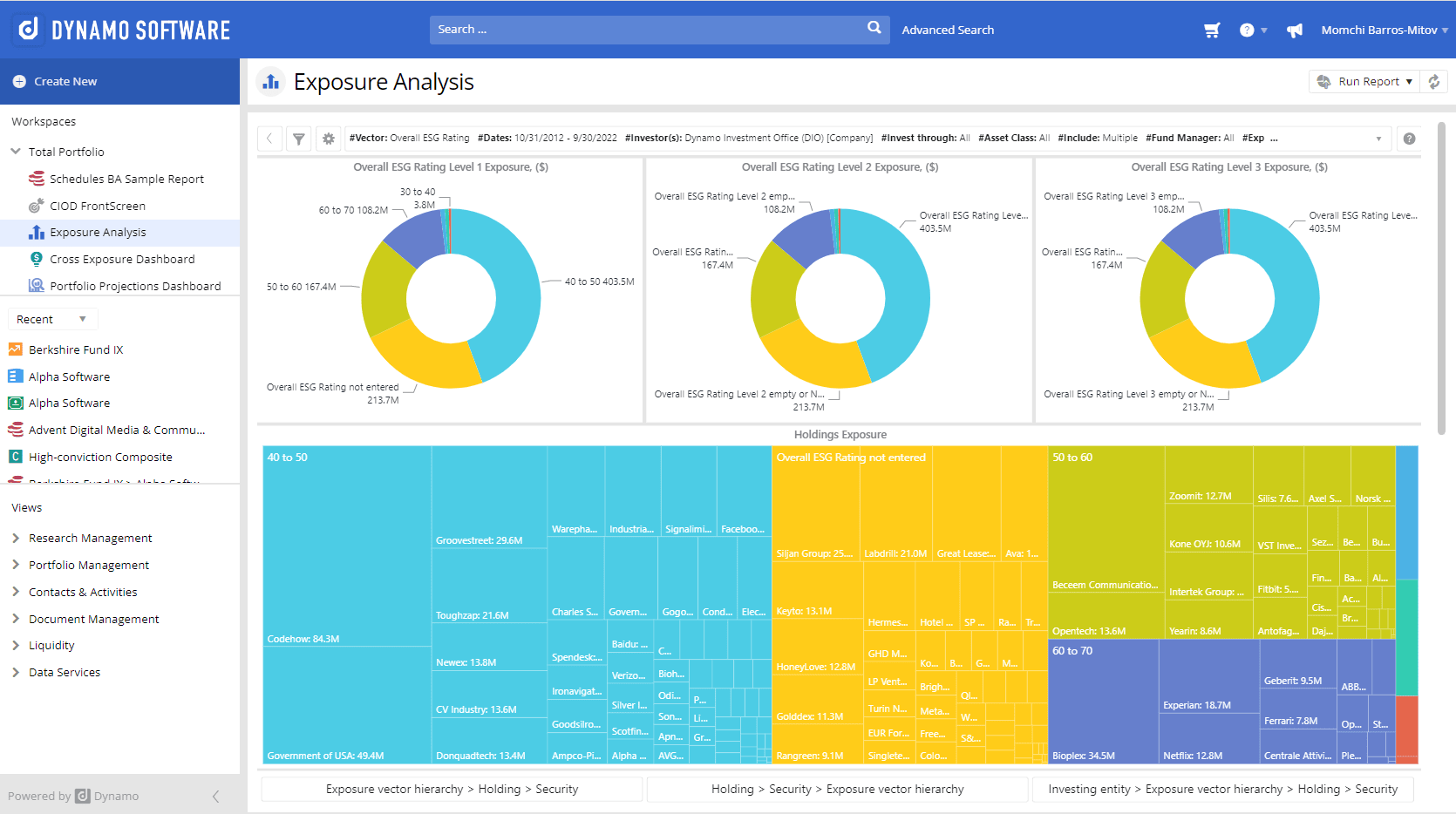

Dynamo Software and CSRHub Partner to Integrate ESG Risk Management Tool Into Alternatives Asset Management Platform

By CSRHub Blogging

Nov 10, 2022

•

2 min read

ESG App Development, Corporate Sustainability Metrics, ESG Metrics Research, ESG Data Partnerships

CSRHub ESG Data Integrates with HubSpot

By CSRHub Blogging

Nov 01, 2022

•

4 min read

ESG ratings, ESG Investing, ESG App Development, Corporate Sustainability Metrics, ESG Data Partnerships

CSRHub Announces CSRHub ESG Ratings on Salesforce AppExchange, the World's Leading Enterprise Cloud Marketplace

By CSRHub Blogging

Sep 20, 2022

•

2 min read

ESG App Development, Corporate Sustainability Metrics, ESG Metrics Research, ESG Data Partnerships

CSRHub Partners with Rhetorik to Integrate ESG Ratings to CRMs

By CSRHub Blogging

Sep 08, 2022

•

4 min read

Bahar Gidwani, ESG Investing, Corporate Sustainability Metrics, ESG Metrics Research, ESG Data Partnerships

CSRHub Adds Data-Driven ESG Signals from GaiaLens

By Bahar Gidwani

Prev

All posts

Next